The "PR Gap" in Medicine: Why Your Social Media "Breakthrough" Isn't a Cure (Yet)

We are living in an era of viral science. But as funding dries up and

What Nigeria's capital funding collapse means for African healthtech, and why the companies filling the gap are building a private healthcare system from the ground up.

On February 10, 2026, Nigeria's Coordinating Minister of Health, Muhammad Ali Pate, stood before the House of Representatives Committee on Healthcare Services to defend the ministry's 2026 budget. During the session, he disclosed a figure that should have triggered a national conversation but instead passed through the news cycle in 48 hours.

Out of ₦218 billion appropriated for health capital projects in 2025, only ₦36 million was released.

₦36 million is roughly what it costs to buy two mid-range SUVs in Lagos. This was the entire capital release for health infrastructure in a country where the WHO recommends a doctor-to-patient ratio of 1:600, and where 43,221 health workers migrated abroad between 2023 and 2024, a 200% surge across all cadres, according to the Federal Ministry of Health's own statistics report.

This is not new. But the trajectory is new. And the trajectory changes the investment thesis.

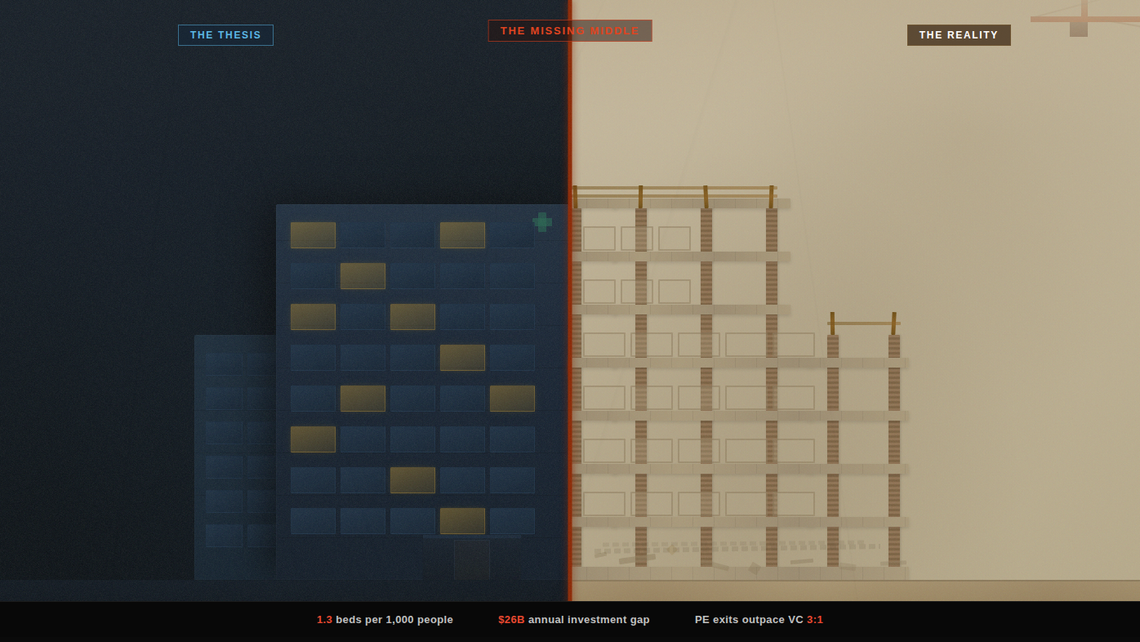

A skeleton without skin is a museum exhibit. Skin without a skeleton is a shape that cannot stand. The skeleton is the hard infrastructure of a health system: the hospitals, the cold chains, the power grids, the roads that connect a warehouse in Lagos to a clinic in Sokoto. The skin is everything the patient touches: the app, the telemedicine call, the insurance card, the pharmacy counter. Most of the global conversation about African healthtech is about the skin. This piece is about the skeleton, and what happens when no one is building it.

In Part 1 of this series, I laid out the case for "tech plus assets" as the real healthtech play in Africa. The argument was structural: you cannot disrupt a sector that has not been built yet, and the exits prove that buyers are paying for physical footprint, not code.

This piece examines what happens to that thesis when the government stops even pretending to build the skeleton. And, perhaps more importantly, why capital keeps flowing into Nigeria anyway.

I wrote in Part 1 about the $26 billion annual infrastructure investment gap identified by the AfDB, and the $4.5 billion African governments actually spend. The 10-year capital release data for Nigeria's health sector tells us something more specific and more alarming: even the money that is allocated is not reaching the ground.

In 2016, ₦28.7 billion was appropriated for health capital projects. 53% was released. Not great, but functional. By 2021, appropriation had jumped to ₦134 billion with 70% released, a brief moment of fiscal seriousness. Then the collapse began: 45% in 2022, 30% in 2023, 15% in 2024. And then the cliff: 0.016% in 2025.

The minister attributed the collapse to the "Bottom-Up Cash Plan" policy operated by the Office of the Accountant General. The Health Sector Reform Coalition was less diplomatic. Their chairman, Mohammed Lecky, said at a press conference on February 14 that if ministries cannot rely on capital releases, long-term projects like hospital upgrades, digital health systems, supply chains, and workforce expansion become impossible.

He is right, but he understated it. What the data shows is not a temporary disruption. It is a structural severance between what the government promises and what it delivers. The appropriation keeps growing (₦218 billion in 2025, up from ₦28.7 billion in 2016). The release keeps shrinking. The gap is not closing. It is widening exponentially.

In Part 1, I argued that the real exits in African healthcare are going to asset-heavy companies. Goodlife Pharmacy sold because it had 150 storefronts. Grinta acquired Citi Clinic to own care delivery. MYDAWA raised $9.6 million to open physical stores.

The ₦36 million data point sharpens that thesis into something harder.

When the government releases 0.016% of its capital budget for health, it is not just failing to build. It is creating a vacuum that the private sector must fill, and in doing so, it is inadvertently handing those private companies an infrastructure moat that no competitor can replicate cheaply.

Consider what this vacuum forces companies to become. Helium Health started as an EMR company. By September 2025, it had disbursed over $10.9 million in collateral-free loans to more than 460 healthcare facilities across 22 states in Nigeria and Kenya. It did this because the facilities could not digitize without financing, and they could not get financing from banks without collateral. Helium provided the hardware, the software, and the credit. That is not a SaaS company. That is a utility. Whether it is a sustainable one remains an open question. Helium is carrying both technology risk and credit risk in an operating environment where either one alone has broken well-funded companies.

LifeBank does not just have an app for blood delivery. It owns oxygen plants and cold-chain motorbikes. DrugStoc and Remedial Health own warehouse infrastructure. These companies are not choosing to be asset-heavy because it is fashionable. They are asset-heavy because the ₦218 billion that was supposed to build the public infrastructure they depend on never arrived.

Here is the part of the analysis that most commentators skip. Despite the capital release collapse, despite the infrastructure tax, despite the brain drain, Nigeria remains the largest addressable healthcare market in sub-Saharan Africa. And the companies operating in it are, in many cases, generating revenue at a scale their East African competitors have not yet matched.

The numbers are straightforward. Nigeria's pharmaceutical market alone is valued at $4.5 billion and growing at 9% annually, according to Pharma West Africa. The broader digital health market reached an estimated $571 million in 2024, with a projected compound annual growth rate of 8.6% through 2029. Nigeria imports over $2 billion in pharmaceutical products annually. That import dependency is a problem, but it is also a revenue opportunity for every company that can shorten or digitize the supply chain between manufacturer and patient.

But there is an important caveat to the capital map above: much of that money is sitting idle. The $14.1 billion figure represents committed capital, not deployed capital. Across the continent, healthcare-focused funds that have successfully raised capital are finding deployment harder than fundraising. The pipeline of companies that meet institutional investment criteria, meaning audited financials, clear unit economics, governance structures, and a path to profitability, is thinner than the capital available to fund them. This is the deployment paradox: the money exists, the need exists, but the infrastructure burden makes companies hard to underwrite. They are too asset-heavy for typical VC, too early-stage for PE, and too commercially oriented for DFI grant funding. The capital is not absent. It is mismatched.

The population math is inescapable. 230 million people, with a median age of 18.1 years. Over 50% of the population still without reliable access to basic health services. The disease burden is enormous, the demand is real, and it is not going away because the government failed to release its capital budget.

Consider the profitability paradox. In a market where the government has stopped funding the backbone of the health system, private companies that deliver reliability command a premium. In the pharmaceutical supply chain, private medicine prices can reach multiples of international reference prices due to fragmented distribution. Companies like mPharma and Remedial Health aggregate demand to offer 30-60% savings to pharmacies and patients while capturing meaningful margins from compressing the value chain. WellaHealth processed ₦1.4 billion in pharmacy benefits by 2024. Helium Health earns on its financing layer on top of its SaaS fees.

These are real revenue figures, not pitch deck projections. For context, a 2024 Tech In Africa analysis found that 85% of Nigerian fintech companies are post-revenue, and 76% are already profitable. Healthtech is structurally earlier stage than fintech, and the comparison is imperfect because healthcare carries higher operating complexity and longer payback periods. But the companies that have crossed the revenue threshold in Nigeria are earning more per transaction than their equivalents in smaller East African markets, where the addressable population is a fraction of the size and the unit economics are structurally lower.

Reliance Health illustrates both sides of this paradox. Before its 2025 restructuring and layoffs, it averaged 3.5x year-on-year revenue growth with a 99% contract renewal rate among corporate clients. That growth was overwhelmingly generated in Nigeria. When it expanded to Egypt and Senegal, the results were, by multiple accounts from former employees, unimpressive. Nigeria was the engine. But the cost of operating in Nigeria, the generators, the parallel logistics, the talent retention against emigration pressure, made reaching breakeven difficult even at that scale. Reliance is not a failure. But it is not yet proof that the model works either. It is proof that the market generates revenue and that the infrastructure tax consumes it almost as fast.

Nigeria is the most extreme case, but it is not the only country grappling with the intersection of infrastructure deficits and healthtech ambition. The relationship between government fiscal discipline, market size, and the type of healthtech company that can be built varies dramatically across the continent. Each market has evolved a distinct strategic model shaped by what the state provides and what it does not.

Nigeria: Infrastructure Substitution. The government has effectively exited capital funding for health. Private companies must build power, logistics, connectivity, and financing alongside their core product. The result is vertically integrated micro-utilities: Helium Health (EMR + lending), LifeBank (logistics + oxygen production), Remedial Health (marketplace + warehousing). The reward is high: scarcity premiums, large addressable market, deep lock-in once you build. The stress is also high: margins are consumed by infrastructure costs, talent emigrates, and the regulatory environment is unpredictable. The jury is still out on whether even the best-funded of these companies can reach sustainable profitability under this model.

Kenya: System Integration. The government invests in shared digital rails: a Digital Health Act (2023), a National Health Information Exchange, and interoperability standards (HL7/FHIR). Founders can build platform companies that plug into government infrastructure rather than replacing it. M-TIBA works as a mobile health wallet because M-Pesa provides universal payment rails. MYDAWA raised $9.6 million to expand physical stores within a system that already has digital foundations. The barrier to entry is lower, but so is the ceiling. The market is roughly one-fifth the size of Nigeria's, and the plug-and-play model means competitors can replicate faster.

Rwanda: Centralized Partnership. Over 90% health insurance coverage through Mutuelle de Sante. OOP spending below 10%. The government is the primary customer. Zipline operates nationwide drone delivery under long-term government contracts with guaranteed payment. The operating environment is predictable. The trade-off: the total market is small, companies are dependent on a single buyer, and government priorities can shift abruptly.

Egypt: Platform-to-Care Pivot. The ecosystem began with platform plays: Vezeeta (13,000+ providers, 3 million appointments annually), Yodawy (e-pharmacy), Chefaa (prescriptions). But Grinta's 2025 pivot is the signal: it exited B2B pharmaceutical distribution entirely to acquire Citi Clinic (150,000+ patients) and shift to direct care delivery. Large centralized urban market, growing manufacturing base, but OOP at roughly 62% creates dynamics similar to Nigeria in a more connected operating environment.

Ghana: The Capital Trap. The government allocated GHS 27.7 billion to health in 2025, but capital spending was 61% lower than budgeted while employee compensation exceeded targets by 17%. The recurrent budget eats the capital budget. mPharma, headquartered in Accra, has responded by building the pharmacy-as-primary-care model, expanding into Francophone Africa where it reached $1.5 million annualized revenue in seven months.

South Africa: The Equity Bridge. Health spending is roughly 8.5% of GDP, budget execution is around 90%, OOP is in the single digits. The infrastructure exists. The challenge is equity: a world-class private system serves 16% of the population while the public system serves 84%. Healthtech companies here build devices, diagnostics, and R&D, not logistics workarounds.

The implication for investors is direct: the type of healthtech company that can succeed depends almost entirely on what the government in that market actually delivers. In Kenya, you can build a platform company. The entry is easier, but the reward scales with a smaller population. In Rwanda, you can build a service company under contract. The operating margin is stable, but you are one policy change from losing your market. In Egypt, you build the platform then acquire the care delivery. In Nigeria, you have to build the platform, the service, and the infrastructure underneath both. The reward ceiling is the highest on the continent. So is the probability of running out of capital before you reach it.

When the government releases 0.016% of its health capital budget, the financial burden does not disappear. It transfers to the person who can least afford it.

The most recent National Health Accounts report (2023-2024) puts Nigeria's out-of-pocket health expenditure at 58.3% of total health spending. I want to flag this figure because it is significantly lower than the 70-75% commonly cited in older analyses and still widely repeated. The NHA data, produced by the Federal Ministry of Health in collaboration with the National Bureau of Statistics and the WHO, represents the most authoritative current figure. Even at 58.3%, Nigeria's OOP rate remains among the highest on the continent and in the world.

The Multidimensional Poverty Index (2024) classifies 33% of Nigeria's population, roughly 73.7 million people, as multidimensionally poor. Another 16.6% are vulnerable to falling into poverty. A single hospitalization can be the event that tips a household over the edge.

But here is what the OOP data also tells us: 58.3% of total health expenditure is cash flowing directly from patients to providers. In a pharma market worth $4.5 billion and growing at 9% annually, that is over $2.6 billion in annual patient-to-provider cash flow. This is not a theoretical market. It is a functioning, if brutal, payment system. The companies that can reduce the cost of each transaction while capturing a margin on the intermediation are building real businesses.

This is the fundamental tension at the bottom of the pyramid. The 73.7 million multidimensionally poor Nigerians are not a subscription market. They are a pay-per-crisis market with extremely price-sensitive consumers. The healthtechs that have found a way to serve them are not selling apps. They are compressing supply chains, providing embedded finance to facilities, offering micro-insurance through pharmacy agent networks, or running pay-for-performance logistics. Every one of these models involves owning or controlling a physical asset.

There is a structural cost to the asset-heavy model that I have not seen adequately discussed: fragmentation.

When every company must build its own power, logistics, and connectivity stack, network effects evaporate. Data does not flow between systems. Patients cannot transfer records from one provider to another. Less than 18% of Nigerian hospitals use electronic medical records, and among those that do, most systems are proprietary and non-interoperable.

This fragmentation is not a choice. It is a survival mechanism. When the government provides no shared digital backbone, every company builds its own. The result is that Nigeria's healthtech ecosystem, despite its size and energy, lacks the connective tissue that makes markets like Kenya more efficient per dollar deployed.

In Part 1, I wrote about the "missing middle" in funding. There is also a missing middle in infrastructure: the shared rails, interoperability standards, common data formats, and trusted identity layers that would allow individual companies to specialize instead of vertically integrating everything. Kenya's Digital Health Act and India's Ayushman Bharat Digital Mission demonstrate that government investment in digital public infrastructure, even modest investment, unlocks disproportionate private sector efficiency.

Nigeria's 0.016% capital release rate means that investment is not coming any time soon. Which means the fragmentation will persist, and the companies operating within it will continue to bear costs that their East African competitors do not.

There is a strategic option that the Nigerian healthtech ecosystem has largely ignored: collaboration between competitors.

If the government is not going to build the shared rails, and no single company can afford to build them alone, then the logical next step is for companies to build them together. This is not idealism. It is arithmetic. When five companies each spend 25% of their operating budget maintaining separate generator-powered server infrastructure, separate last-mile logistics fleets, and separate cold chains, the aggregate waste is staggering. The same capital pooled into shared logistics corridors, interoperable data standards, or collective purchasing agreements would unlock efficiencies that individually no one can reach.

There are early precedents elsewhere. India's Unified Payments Interface (UPI) was built through a consortium model: competing banks agreed on shared rails that reduced costs for everyone while still competing on the product layer above. Kenya's M-Pesa ecosystem functions similarly. Even in Nigerian fintech, the Nigeria Inter-Bank Settlement System (NIBSS) provides shared infrastructure that no single bank could have built alone.

Healthcare needs its equivalent. A shared cold chain network that multiple pharmaceutical distributors can access. An interoperable patient identity layer that EMR companies agree to support. A collective logistics pool for last-mile delivery in underserved states. These are not competitive advantages for any single company. They are pre-competitive infrastructure that would allow every company to compete more effectively on top of them.

The barrier is trust, and it is a real one. In a market where survival is not guaranteed, sharing infrastructure with a competitor feels like handing them a weapon. But the alternative is what we have now: an ecosystem where everyone is building everything from scratch, margins are thin, and the government has made it clear it is not coming to help. Co-opetition is not a soft concept here. It is a survival strategy.

The "tech plus assets" thesis from Part 1 is not wrong. If anything, the 2025 budget data makes it more urgent. When the government is releasing 0.016% of its health capital budget, the private sector is the only actor left on the field. The companies building physical infrastructure, owning supply chains, financing facilities, and operating logistics: those are the companies that will generate exits.

But I want to add three caveats that I think are important for intellectual honesty.

First, the thesis is self-limiting in Nigeria but self-generating in revenue. The infrastructure tax makes scaling expensive. The OOP-driven revenue model limits the addressable market. The fragmentation prevents network effects. But the sheer size of the market, the scarcity premium on reliability, and the absence of government competition mean that the companies which survive can build genuinely profitable businesses. The question is whether those businesses can scale beyond Nigeria, and the evidence so far suggests that is harder than it looks.

Second, the continent is not one market. A Nigerian founder's playbook will not work in Kenya, where the government has built digital rails. A Kenyan founder's playbook will not work in Egypt, where the urban density and manufacturing base create different opportunities. A Rwandan model, dependent on government contracts, will not work in Nigeria, where the government cannot reliably pay. The strategic model cards above are not rankings. They are different games being played on different boards.

Third, we should not confuse resilience with a model. The companies surviving in Nigeria's environment are impressive. But they are surviving a failure, not operating within a system. The ₦36 million figure is a scandal, not a feature. The private sector is filling a vacuum that should not exist. Celebrating the moat that vacuum creates risks normalizing a fiscal failure that costs lives.

I have spent most of this piece describing the problem. I owe the reader an attempt at direction, even if the honest answer is that there is no clean solution.

What would actually help:

The most dangerous risk is not that the government remains absent. It is that the government returns as a competitor. Nigeria has a history of launching state-owned enterprises and public-private partnerships that compete directly with the private companies that filled the vacuum during the state's absence. If the government decides to build a national digital health platform, or to mandate interoperability standards that advantage a politically connected provider, companies that spent years and millions building proprietary infrastructure could find themselves undercut by a subsidized competitor that does not need to be profitable.

This is not theoretical. The Basic Health Care Provision Fund (BHCPF), established in 2014, was designed to channel 1% of consolidated revenue to primary healthcare. It has been chronically underfunded and poorly disbursed. But if a future administration decides to fully fund it and route payments through a single government platform, every private primary care company in the country becomes a subcontractor overnight, on terms it did not negotiate.

There is also PPP risk. Nigeria's track record on honouring public-private partnership contracts is, to be generous, inconsistent. Companies that enter long-term infrastructure agreements with state or federal government agencies face the real possibility of delayed payments, unilateral contract modifications, or outright non-renewal when administrations change. The lesson from sectors like power generation, where private investors have billions in stranded assets due to government non-payment, should not be ignored by healthtech founders considering PPP models.

And there is a subtler risk: brain drain acceleration. If the operating environment continues to deteriorate, the very talent these companies need to execute, the doctors, nurses, pharmacists, and engineers, will continue emigrating. You cannot build a health system, public or private, without health workers. The 43,221 who left between 2023 and 2024 are not a one-time shock. They are a structural bleed that compounds annually.

At the beginning of this piece, I wrote that a skeleton without skin is a museum exhibit, and skin without a skeleton is a shape that cannot stand. Nigeria's 2025 budget data confirms what many in the industry already knew: the government has abandoned the skeleton. The ₦36 million released is not a budget. It is an admission that the state has opted out of building the structural body of its own health system.

What is left is a country full of companies trying to be both skeleton and skin at once. They are pouring concrete for the bones, cold chains, power systems, logistics corridors, while simultaneously stretching the skin of apps, platforms, and insurance products over the top. It is an extraordinary act of construction. It is also an extraordinarily expensive one, and the capital markets have not yet figured out how to price it.

The question from Part 1 remains: will the funding infrastructure evolve fast enough to support companies that are building physical health infrastructure with venture-scale capital? The 2025 budget data makes that question more urgent than when I first wrote it. Because every year the skeleton goes unbuilt by the state, the private sector calcifies further into a shape it was never designed to hold.

There is no scenario in which this ends well without at least two things happening simultaneously: the private sector organizing around shared infrastructure instead of duplicating it, and the capital markets developing instruments that match the actual risk and return profile of these companies. Neither of those things is happening at sufficient speed. Both are within the control of actors who are currently in the room.

· · ·

Sources and further reading:

Federal Ministry of Health and Social Welfare budget defence disclosures, February 2026 · National Health Accounts 2023-2024 · Partech Africa 2025 VC Report · Africa: The Big Deal · Nigeria Health Statistics Report 2024 · World Bank Global Health Expenditure Database · WHO Health Workforce Statistics · Nigeria Health Watch · Wariri et al., "Understanding the exodus," Global Health Action, 2024 · Health Sector Reform Coalition press conference, February 2026 · Budget Office of the Federation · Pharma West Africa market overview · Statista Digital Health Nigeria · Tech In Africa, "Nigeria's Fintech Sector," December 2025 · NotADeepDive, "Layoffs at Reliance Health," August 2025 · AVCA 2024 African Private Capital Activity Report

Research-driven writing on healthcare, technology, policy, and the systems that shape care across Africa.

Member discussion